Auditors assess financial records and compliance to ensure accuracy and transparency while auditees provide necessary documentation and explanations to facilitate the audit process. Understanding the dynamic between auditors and auditees is crucial for effective risk management and regulatory adherence; explore more insights in this article.

Table of Comparison

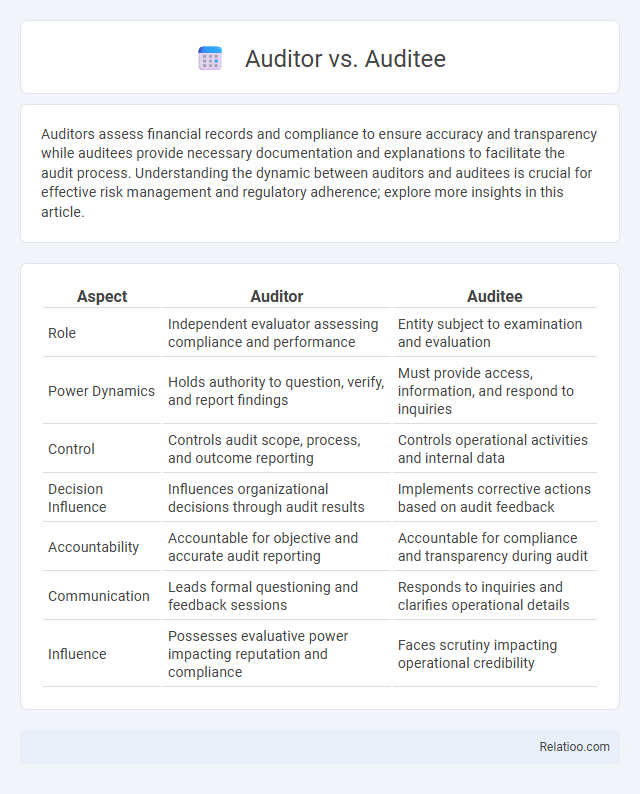

| Aspect | Auditor | Auditee |

|---|---|---|

| Role | Independent evaluator assessing compliance and performance | Entity subject to examination and evaluation |

| Power Dynamics | Holds authority to question, verify, and report findings | Must provide access, information, and respond to inquiries |

| Control | Controls audit scope, process, and outcome reporting | Controls operational activities and internal data |

| Decision Influence | Influences organizational decisions through audit results | Implements corrective actions based on audit feedback |

| Accountability | Accountable for objective and accurate audit reporting | Accountable for compliance and transparency during audit |

| Communication | Leads formal questioning and feedback sessions | Responds to inquiries and clarifies operational details |

| Influence | Possesses evaluative power impacting reputation and compliance | Faces scrutiny impacting operational credibility |

Introduction to Auditor and Auditee

An auditor systematically examines financial records and operational processes to ensure accuracy, compliance, and risk management within an organization. The auditee, typically the entity being reviewed, provides relevant documents and responses to facilitate transparent evaluation by the auditor. Oversight involves ongoing monitoring mechanisms that ensure auditors maintain objectivity and adhere to regulatory standards throughout the audit process.

Definition of Auditor

An Auditor is a qualified professional responsible for examining financial records, compliance, and operational processes to ensure accuracy and adherence to established standards. Your organization relies on Auditors to provide independent assessments that identify risks, irregularities, and opportunities for improvement. Oversight refers to the supervisory framework ensuring both the Auditor's and Auditee's accountability and transparent execution of auditing procedures.

Definition of Auditee

The auditee is the individual, department, or organization subject to the audit, responsible for providing accurate and complete information to the auditor during the evaluation process. Unlike the auditor, who conducts the examination and verification of financial records or processes, the auditee facilitates access to necessary documents and evidence to ensure audit objectives are met. Oversight refers to the broader supervisory function that ensures compliance, accountability, and effectiveness within the audited entity, often involving regulators or governing bodies monitoring both auditor and auditee activities.

Key Responsibilities of an Auditor

An auditor is responsible for examining financial records, ensuring compliance with regulatory standards, and evaluating internal controls to identify risks and discrepancies. Key responsibilities include conducting audits systematically, verifying accuracy of financial statements, and providing objective assessments to support organizational transparency. Auditors also communicate findings to stakeholders while maintaining independence and adherence to professional ethics.

Key Responsibilities of an Auditee

An auditee is responsible for providing accurate and complete documentation, ensuring compliance with established policies, and facilitating access to relevant records and personnel during the audit process. They must implement corrective actions based on audit findings to improve internal controls and operational efficiency. Maintaining transparency and cooperation with auditors supports a thorough and effective evaluation.

Core Differences Between Auditor and Auditee

Auditors objectively evaluate financial records and compliance to ensure accuracy and adherence to regulations, while auditees are responsible for providing accurate data and facilitating the audit process. Oversight involves continuous monitoring and governance by regulatory bodies or internal committees to maintain accountability beyond the audit scope. Core differences lie in the auditor's role as examiner and verifier, contrasting with the auditee's role as subject and data provider.

Importance of the Auditor-Auditee Relationship

The auditor-auditee relationship is crucial for ensuring transparency, accuracy, and compliance in the audit process, fostering trust and effective communication between both parties. A cooperative dynamic enables the auditor to identify risks and control weaknesses while allowing the auditee to provide necessary documentation and explanations, facilitating timely issue resolution. Oversight functions depend heavily on this relationship to uphold standards, enhance accountability, and improve organizational governance.

Common Challenges in Auditor-Auditee Interactions

Communication barriers often arise between auditors and auditees, leading to misunderstandings regarding compliance requirements and audit findings. Your ability to maintain transparency and open dialogue helps mitigate resistance and defensive reactions during the audit process. Oversight bodies face challenges in balancing thorough scrutiny with fostering cooperative relationships to ensure effective audit outcomes.

Best Practices for Effective Audits

Effective audits require clear roles: auditors objectively assess compliance and risks using standardized checklists and evidence-based methods, while auditees prepare through thorough documentation and transparent communication. Best practices emphasize regular training, fostering collaborative environments to address findings constructively, and leveraging oversight bodies to ensure accountability and continuous improvement. Consistent application of auditing standards such as ISO 19011 enhances reliability, promotes trust, and drives organizational excellence.

Conclusion: Enhancing Audit Success

Effective communication between the auditor, auditee, and oversight bodies is crucial for audit success. You can enhance audit outcomes by fostering transparency, ensuring compliance, and addressing findings promptly. Collaboration among these entities strengthens accountability and drives continuous improvement in organizational processes.

Infographic: Auditor vs Auditee