SIP investments enable disciplined wealth creation through regular contributions, while lump sum investments rely on timing the market for potential immediate gains. Explore this article to understand which strategy suits your financial goals best.

Table of Comparison

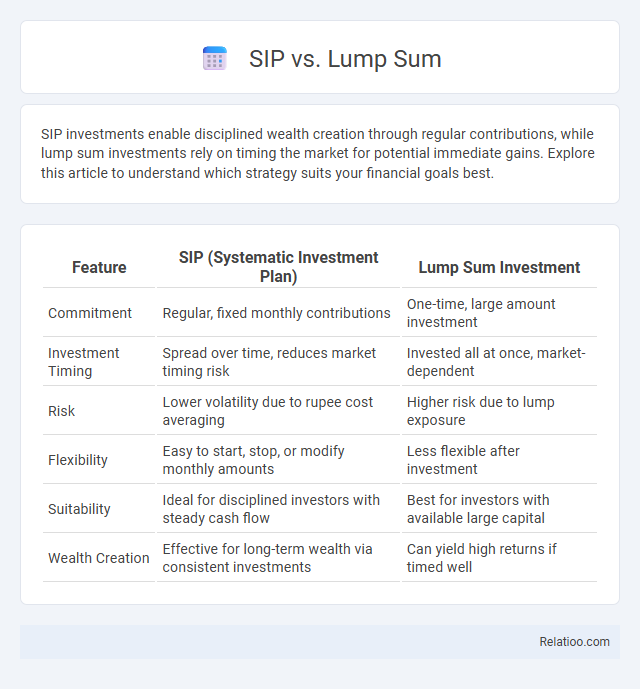

| Feature | SIP (Systematic Investment Plan) | Lump Sum Investment |

|---|---|---|

| Commitment | Regular, fixed monthly contributions | One-time, large amount investment |

| Investment Timing | Spread over time, reduces market timing risk | Invested all at once, market-dependent |

| Risk | Lower volatility due to rupee cost averaging | Higher risk due to lump exposure |

| Flexibility | Easy to start, stop, or modify monthly amounts | Less flexible after investment |

| Suitability | Ideal for disciplined investors with steady cash flow | Best for investors with available large capital |

| Wealth Creation | Effective for long-term wealth via consistent investments | Can yield high returns if timed well |

Introduction to SIP and Lump Sum Investing

Systematic Investment Plan (SIP) allows you to invest a fixed amount regularly in mutual funds, promoting disciplined investing and rupee cost averaging to reduce market volatility impact. Lump sum investing involves putting a large amount into a mutual fund or asset at once, potentially benefiting from market rallies but carrying higher timing risk. Your choice between SIP and lump sum depends on your investment horizon, risk tolerance, and market conditions.

Key Differences Between SIP and Lump Sum

SIP (Systematic Investment Plan) involves investing a fixed amount regularly, promoting disciplined investing and rupee cost averaging, while Lump Sum requires investing a large amount at once, ideal for market timing. SIP reduces the risk of market volatility by spreading investments over time, whereas Lump Sum can potentially yield higher returns if invested during a market dip. SIP suits conservative investors seeking steady wealth creation, whereas Lump Sum benefits those with substantial capital and high-risk tolerance.

How SIP Works: Process and Benefits

Systematic Investment Plan (SIP) works by allowing you to invest a fixed amount regularly into mutual funds, usually monthly, promoting disciplined saving and rupees cost averaging. Each installment buys units at varying market prices, reducing the impact of market volatility and potentially enhancing long-term returns. SIP benefits include convenience, flexibility in investment amount and tenure, and the power of compounding, enabling your wealth to grow steadily over time.

Understanding Lump Sum Investment Strategy

Lump sum investment involves allocating a significant amount of capital at one time into a particular asset or portfolio, aiming to maximize returns by capitalizing on market opportunities immediately. This strategy contrasts with Systematic Investment Plans (SIP), where investments are made regularly in smaller amounts, reducing the impact of market volatility through rupee cost averaging. Understanding lump sum investment requires analyzing market conditions, investor risk tolerance, and time horizon to determine if deploying capital at once can outperform periodic investments over the long term.

Risk Factors: SIP vs Lump Sum

Systematic Investment Plans (SIPs) spread risk over time by investing a fixed amount regularly, reducing the impact of market volatility through rupee cost averaging, while lump sum investments expose the entire capital to market timing risk at once, potentially leading to higher losses during downturns. SIP minimizes the risk of investing a large amount at a market peak, making it suitable for risk-averse investors seeking steady wealth accumulation. Conversely, lump sum investments can yield higher returns in a rising market but involve greater exposure to short-term fluctuations and timing risks.

Suitability: Who Should Choose SIP or Lump Sum?

Systematic Investment Plans (SIPs) suit investors seeking disciplined, long-term wealth creation with gradual market exposure and risk mitigation through rupee cost averaging. Lump sum investments are ideal for individuals with substantial capital ready to capitalize immediately on market opportunities or time-sensitive investments. Risk-averse beginners and those with limited funds benefit more from SIPs, while experienced investors confident in market timing might prefer lump sum options.

SIP vs Lump Sum: Impact on Returns

SIP (Systematic Investment Plan) offers the advantage of rupee cost averaging, reducing the impact of market volatility by investing a fixed amount regularly, which can lead to more stable returns over time. Lump sum investment allows for the possibility of higher returns if invested during market lows but carries greater risk due to market timing dependency. Historical data shows that SIPs perform better in volatile markets, while lump sum investments can outperform during prolonged market uptrends.

Tax Implications: SIP and Lump Sum Investments

Systematic Investment Plans (SIPs) and lump sum investments both offer distinct tax implications that affect Your overall returns. SIPs generally provide the advantage of rupee cost averaging, potentially reducing tax liability over time through staggered investments in equity-linked savings schemes (ELSS) which qualify for tax deduction under Section 80C up to Rs1.5 lakh annually. Conversely, lump sum investments locked in ELSS also qualify for Section 80C deductions but may lead to a larger short-term capital gains tax if withdrawn before the lock-in period of three years.

Market Timing: Is It Relevant for SIP and Lump Sum?

Market timing plays a critical role in lump sum investments, as entering the market at a peak can significantly impact returns, whereas Systematic Investment Plans (SIPs) mitigate this risk through rupee-cost averaging by investing fixed amounts periodically regardless of market conditions. SIPs reduce the pressure of timing the market, smoothing out volatility over time, making them ideal for investors seeking disciplined, long-term growth without the need to predict market highs or lows. Your investment strategy should consider your risk tolerance and time horizon, with lump sum investments favored when confident in market entry points and SIPs preferred for consistent accumulation despite market fluctuations.

Conclusion: Choosing the Best Investment Approach

You should evaluate your financial goals, risk tolerance, and investment horizon when choosing between SIP, lump sum, and other investment options. SIP offers disciplined, regular investing with rupee cost averaging, while lump sum suits those with immediate capital and a higher risk appetite. Matching your investment strategy to your personal needs ensures optimal growth and financial security.

Infographic: SIP vs Lump Sum